5G is here but the challenges are just beginning

Follow article

Dave from DesignSpark

Dave from DesignSpark

How do you feel about this article? Help us to provide better content for you.

Dave from DesignSpark

Thank you! Your feedback has been received.

Dave from DesignSpark

There was a problem submitting your feedback, please try again later.

Dave from DesignSpark

What do you think of this article?

The long-awaited 5G roll-out has begun and it seems as if every month brings announcements of accelerated roll-out plans. In the US, AT&T and Verizon were the first to market, with both announcing 5G services in the closing months of 2018 and the remaining two major service providers committing to launches by mid-2019. In Asia, 2019 has seen 5G arrive in South Korea, Japan and China and, around Europe, the first commercial 5G subscriptions are also expected during 2019.

Implementing the full range of 5G capabilities requires significant investments by operators, representing a tricky balancing act as this cash has to be found before 5G revenues start to flow. At the same time, many operators are still building out 4G/LTE networks whilst many are seeing revenues dip as existing services become commoditised.

The path to 5G profitability, therefore, requires a strategic plan, taking account of factors such as the technology roadmap, the evolving regulatory landscape and, of course, local/regional market opportunities. This article reviews some of these factors and looks at how operators are adapting their roll-out plans to balance their investments against 5G revenue streams.

The 5G roll-out is underway

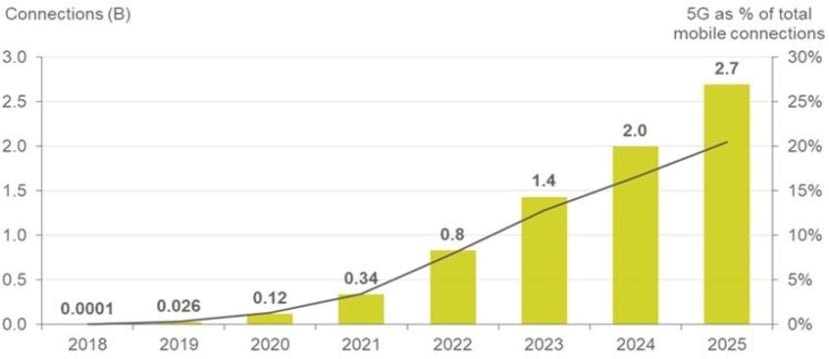

Although in the short term, 5G deployment may pose challenges to mobile operators, market demand and the consequent opportunities are driving an acceleration of global roll-out plans. From a standing start in late 2018, 5G subscription uptake is expected to be faster than any other mobile communication technology so far, with CCS Insight, a UK market research company, forecasting that global 5G connections will reach 2.7 billion by 2025, Figure 1.

Figure 1: Forecast growth in global 5G connections (Source: CCS Insight)

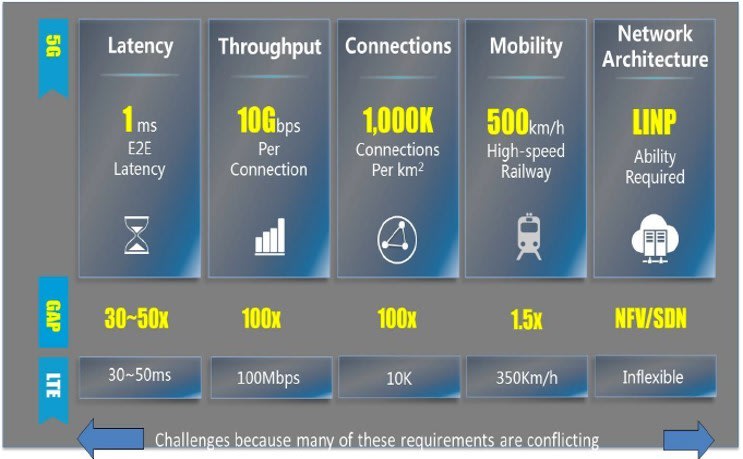

The term 5G Service, however, covers a wide spectrum of network capabilities, as can be seen from the International telecommunication Union’s, (ITU), requirements specification, IMT2020, Figure 2.

Figure 2: 5G performance requirements (Source: NGMN 5G White Paper)

To meet these requirements operators must invest heavily in all network domains, including spectrum, radio access network (RAN) infrastructure, transmission, and core networks. According to a study of one European country by McKinsey & Company[i], a management consultant, network capital expenditure may have to increase by 60% over the period 2020 to 2025, equating to an approximate doubling of the total cost of ownership.

It would not be surprising, given the above, to find most operators adopting an evolutionary approach to 5G roll-out, balancing investments against incremental revenues. The roadmap for global 5G service availability is therefore dependent upon how operators prioritise their investments, based on local regulatory and market conditions.

Regulatory and Technical Factors

As with any wireless networking technology, availability of spectrum is a key enabler of 5G, which will make use of frequencies ranging from 0.4 GHz up to the mmWave frequencies at 30GHz and above. The capabilities offered by 5G services will be based on the transmission frequencies used, with the “holy grail” of fast speeds and high bandwidth being unlocked by mmWave network technologies.

The design and implementation of mmWave networks are both technically challenging and costly to implement; innovative low-power RF amplifiers which can operate efficiently at these frequencies are required, and the transmission characteristics of signals at these frequencies require massive densification of networks.

Recognising these challenges, 3GPP, the global body responsible for developing 5G standards, focused on 5G NR non-Stand-Alone (NSA) technology in its first release covering 5G (Release 15). 5G NSA enables operators to leverage existing 4G/LTE infrastructure to offer services, by upgrading with massive MIMO technology.

A review of roll-out plans around the world would suggest that the majority of operators are following this approach, as illustrated by the sample summarised in Table 1. With the exception of AT&T and Verizon, who are using their mmWave spectrum to offer home broadband services in targeted cities, most other operators appear to be focusing initially on the “mid-range” sub-6 GHz frequencies, the so-called “sweet spot” for MIMO. These operators are initially concentrating on consumer offerings, working with manufacturers of mobile devices to offer faster download speeds. In the UK, EE and Vodafone have also indicated an intent to offer fixed wireless access (FWA) in rural areas.

|

Operator |

Frequencies |

Services |

|

AT&T |

39 GHz |

Home Broadband |

|

Verizon |

28/39 GHz |

Home Broadband |

|

T-Mobile (USA) |

600 MHz |

Consumer, handsets, tablets, etc. |

|

EE |

3.4 GHz |

Consumer, handsets, tablets, etc. |

|

Vodafone |

3.4 GHz |

Consumer, handsets, tablets, etc. |

|

China Unicom |

3.5 – 3.6 GHz |

Consumer, handsets, tablets, etc. |

|

South Korea (all 3 operators) |

3.5 GHz |

Consumer, handsets, tablets, etc. |

Table 1: Sample launch plans

These are short-to-mid-term strategies, enabling early market entry and revenue realisation whilst delaying the investments required to build out the full 5G infrastructure. However, even though many countries are currently auctioning spectrum in the mid-range, it is a finite resource and will eventually run out, by 2025, according to McKinsey.

Two events in 2019 are likely to trigger the next wave of spectrum auctions and investments in 5G networks; In October, at its 4-yearly World Radio Conference (WRC) the ITU will finalise spectrum allocations for 5G and, by December, 3GPP is scheduled to deliver Release 16, completing the 5G specifications including the standards for mmWave 5G.

Market Drivers

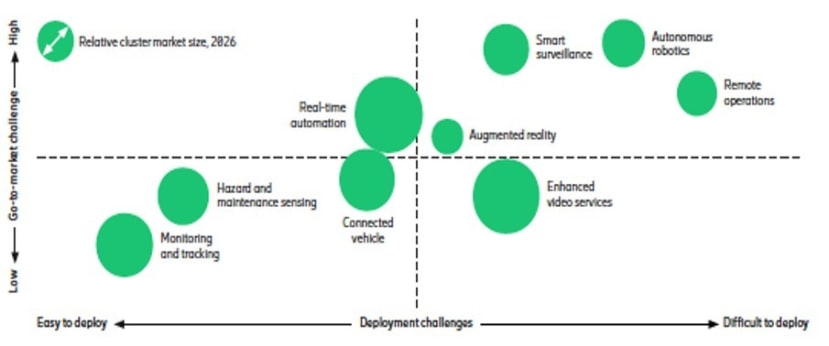

Most current 5G roll-out plans can be considered to be targeting the “low-hanging fruit”, addressing consumer demand for more bandwidth whilst minimising the need to make significant network investments. The real revenue opportunities, however, will come when 5G capabilities can unlock the latent demand of a range of applications across multiple verticals. 5G will be a major enabler of digitalisation across industries such as agriculture, retail, automotive, manufacturing and energy and utilities and, according to a recent study by Ericsson and A.D. Little[ii], by enabling the use cases for these applications, operators can expect to see a revenue uplift of as much as 36% by 2026.

Needless to say, however, unlocking these revenues requires investment in the next level of 5G networks. Autonomous vehicles and cloud robotics, for example, will require the levels of latency that can only be achieved through the widespread implementation of edge computing. Likewise, the realisation of smart city applications involving thousands of sensors in a compact geographical area will require network densification. Figure 3 shows a mapping of typical use cases against ease of deployment and go-to-market challenges, proxies for investment requirements.

Figure 3: Application Growth Opportunities (Source: The Guide to Capturing the 5G Industry Digitalisation Business Potential, Ericsson)

Disruption Lies Ahead

The enhanced network performance of 5G, with its step changes in download and upload speeds, as well as ultra-low latencies, promises to be a key driver of industry digitalisation, disrupting many existing business models and creating both opportunities and threats, not just for mobile operators but for players in industries as diverse as gaming and automobiles.

Operators and equipment manufacturers in the telecoms industry are already aligning themselves, forming eco-systems to address emerging demands. The 5GAA association, for example, has evolved to ensure that the requirements of the autonomous automobile market are captured in the evolving 5G specifications. Similarly, OneM2M aims to create standards and solutions for emerging Machine-to-Machine and IoT technologies.

As 5G takes off, successful players will need to survive in and manage eco-systems of increasing complexity. To reap the benefits of industry digitalisation, for example, operators must build go-to-market partnerships with industry specialists, application developers, and systems integrators. Innovative approaches to managing investments will also be required, requiring the concept of sharing of 5G networks to be carefully explored.

As with any emerging, disruptive, technology, there will be winners and losers, with agility, innovation, and collaboration being key enablers of success.

Conclusion

5G services are now available in many countries but, for the most part, are being provided over enhanced LTE networks, using mid-range spectrum in the sub-6 GHz range. Whilst these services enable operators to demonstrate a 5G capability, the real opportunities will only be unlocked when the full 5G network functionality is available, requiring significant investments across all network domains. To unlock the benefits predicted from the digitalisation of industry, operators will need to carefully target investments and work within complex eco-systems to access their chosen market segments.

[i] The Road to 5G: the inevitable growth of infrastructure cost, McKinsey & Company

[ii] The 5G Business Potential, Second Edition, Ericsson

Comments